Editor’s note: This is the third article in a fall financial series of New Dentist Now blog posts from Darien Rowayton Bank, which provides student loan refinancing and is endorsed by the American Dental Association. Qualifying ADA members receive a 0.25% rate reduction to DRB’s already low rates for the life of the loan as long as they remain ADA members. View rates, terms and conditions and disclosures at student.drbank.com/ADA.

If you’re looking into refinancing your dental school loans, you’ll need to choose between variable and fixed-rate loans. There are several factors to keep in mind that aren’t immediately obvious, so let’s break down each type of loan.

Variable Rates

Variable Rates

A variable-rate loan is exactly what you might expect: a loan where the interest rate can move up or down over time. But what exactly causes them to be variable? Variable rates are generally pegged to LIBOR (the London Interbank Offered Rate), which is the average interest rate one major bank will charge another major bank when borrowing.

As it happens, LIBOR has been at near-historic lows for the last few years, since the financial crisis in 2009, translating into correspondingly low variable rates that you’ll see when refinancing your dental-school loan. If you look at the offerings of major student lenders, variable interest rate loans are often set a couple of percentage points lower than fixed-rate loans because borrowers are taking on an interest-rate risk in the event that LIBOR rates rise. This means that if you choose a longer repayment term, there’s no guarantee that whatever excellent rate you get today will stay the same in 15 years, or even 5 years.

It’s difficult to imagine that rates will drop much lower than they are now—interest rates will most likely rise in the future. The longer a repayment term you select, the larger the risk that your variable rate will rise during the term of your loan. Some variable-rate loans have caps on how high the interest rate can reach, and it’s definitely worth taking that into account when making your decision.

Fixed Rates

Compare that to a fixed-rate loan. In a scenario where you choose a fixed-rate loan, you accept a slightly higher interest rate now, but are guaranteed that no matter how much those variable interest rates fluctuate, your rate will not change for the life of your loan. It’s a more conservative option than a variable rate and can be a solid choice in certain situations.

What Does It All Mean?

The next step is taking all of this into account and figuring out how it should affect your own student-loan refinancing. Since variable rates are lower now and are likely to rise in the future, a variable loan is probably a good choice if you are planning on repaying your loan off quickly, and if you are in a good position to take on some interest-rate risk.

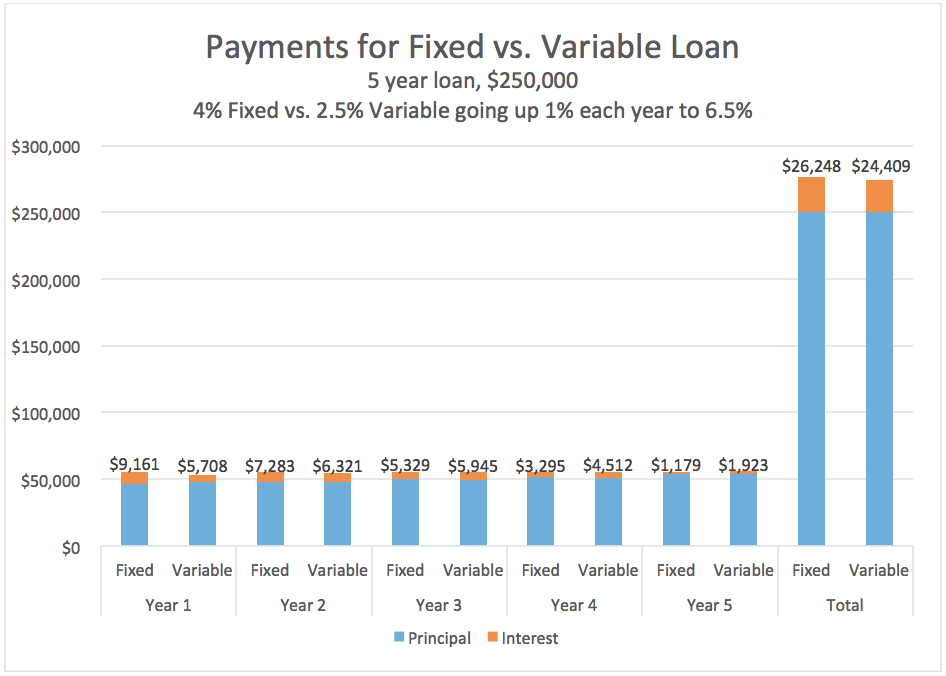

Let’s look at the case of a newly minted dentist (with a starting salary of around $180,000). She opts to devote the first few years after graduation to paying off her student loans as quickly as possible. After exploring her options, the best fixed-rate she is offered for a 5-year term is 4.0 percent compared to a 2.5 percent variable starting rate. For the purposes of this illustrative example, let’s assume rates move up very quickly such that her variable rate would rise by 1 percent each year, eventually reaching 6.5 percent in year 5:

The chart above illustrates how much the borrower pays each year, broken up into interest and principal (orange and blue). As you can see from the last bar, the borrower paid $1,800 more in interest on the fixed than on the variable. A variable rate is the better choice, even if we assume rates go up 1 percent each year all the way up to 6.5 percent.

Here’s why: In year 1 of the loan, interest makes up a much larger percent of the payment—the principal remaining is high and so is the interest. Over time, however, as principal is paid down, the amount of interest owed goes down such that the interest has a smaller impact to the borrower and to the total amount paid. While this borrower is paying a higher interest rate in years 4 and 5 on the variable-rate plan, the bulk of her original loan has already been paid off, so the interest makes up a smaller percent of her payments this late in the loan. The real savings from choosing the variable rate come at the beginning of the loan, when the lower variable interest rates in years 1 and 2 result in high interest savings that are only partially negated by the higher rates in years 3, 4, and 5.

Ultimately, our dentist saves almost $2,000 by selecting the variable-rate plan because of the lower rates when the loan balance was at its highest. In addition, if rates do not increase as much or are slower to rise than the above example, the interest savings could be even higher for this dentist.

So what’s the conclusion of all this? With rates as low as they currently are, it is a great time for dentists to refinance their student loans. A variable rate may be a good way to save even more, even if rates go up significantly over time.

One big note of caution: The payments on variable-rate loans could go even higher than projected in the chart above. As such, a variable loan should only be taken on by borrowers who expect to have future income that will allow them to make higher payments if rates go up very high and very fast. When making a decision about what type of interest rate to choose, you need to consider how aggressive you can be in repayment, how much risk you are willing to tolerate, and your overall financial situation both now and in the future. If all of those do not align, a fixed-rate student loan refi might be a better option.

About DRB

DRB (Darien Rowayton Bank) is a national bank, marketplace lender, and the fastest lender in industry history to reach $1 billion in student loan refinancings. FDIC insured and established in 2006, DRB Student Loan has helped thousands of professionals with graduate and undergraduate degrees across the country to refinance and consolidate federal and private student loans, saving these borrowers thousands of dollars each.

DRB’s student loan refinancing program has been endorsed by the ADA. For more information about the student loan refinancing program, visit https://student.drbank.com/ADA.